Service is 60% of your corporate profit. Stop treating it like overhead.

The number on the wall

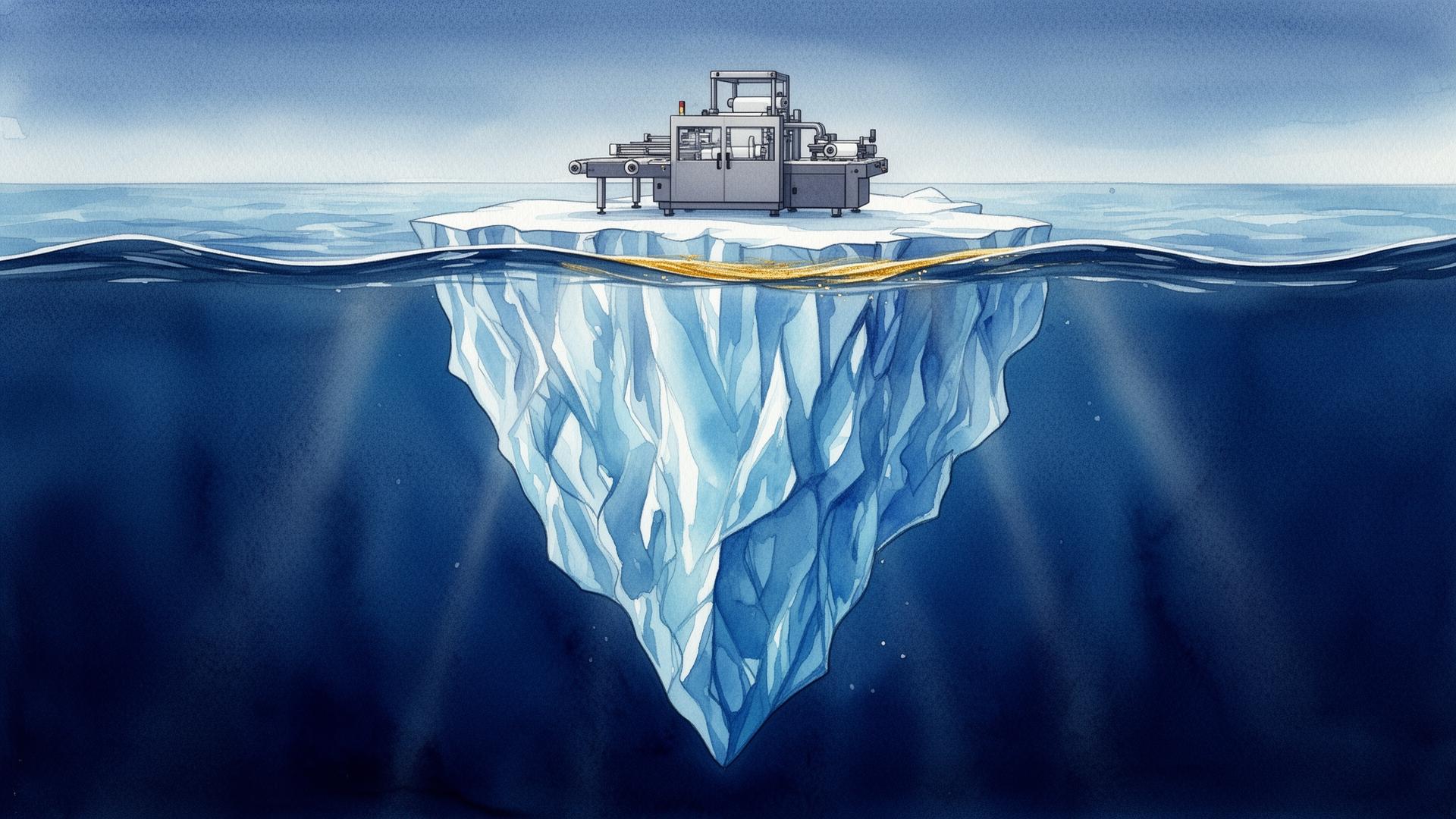

There's a number every capital equipment manufacturer should have on the wall of every executive meeting room.

Most don't.

The number is 60%.

That's the share of total corporate profit that comes from service contracts and aftermarket revenue at mature equipment manufacturers — even though service typically represents only 25–30% of total revenue.

Read that again.

A quarter of the top line generates more than half of the bottom line. And yet in most organizations, service is still managed, budgeted, and staffed like a cost center.

The hidden math

Industry analysis from BCG and Aberdeen Group (via PTC) has been consistent for over a decade:

- New equipment sales: typical margins of 10–15%

- Service contracts, spare parts, training, upgrades: typical margins of 35–50%

The implication is uncomfortable for anyone running a traditional capital equipment P&L: the machine you fought to sell at 12% margin is, in pure economic terms, the customer acquisition cost for the service relationship that follows. The real product is the next 15 years.

Why the smartest manufacturers stopped pretending

The leaders in the category — the ones quietly compounding share — have already restructured around this reality:

- Service is a P&L, not a department.

- Service has its own GM, its own roadmap, its own investment thesis.

- Service contracts are sold alongside the machine, not after it breaks.

- Engineers, technicians, and field experts are treated as revenue producers, not cost lines.

Where the 60% actually comes from

Break the service P&L apart and the structure becomes obvious:

- Service contracts — recurring, predictable, high-margin. The closest thing capital equipment has to SaaS.

- Spare parts — captive market, near-zero customer-acquisition cost, premium pricing power.

- Training & certification — pure-margin knowledge revenue, scales without proportional cost.

- Upgrades & retrofits — extends asset life and locks in the next decade of the relationship.

- Remote support — the multiplier. Reduces cost-to-serve while increasing perceived value.

Each of these compounds. None of them require building a new machine.

The remote support multiplier

The single biggest unlock in the last five years has been remote visual support.

IFS published a case study showing one industrial manufacturer cut truck rolls by 50% through remote triage. That's not a productivity number — it's a margin number. Every truck roll avoided is travel cost eliminated, technician time recovered, response time compressed, and customer downtime reduced.

The math compounds:

- Fewer dispatches → higher gross margin per contract

- Faster resolution → higher renewal rates

- Captured knowledge → lower training cost for new technicians

- Better data → smarter contract pricing

What this means for the next decade

The industrial companies winning the 2030s won't be the ones with the best machines. They'll be the ones with the best service economics.

Three things separate them already:

- They measure service margin, not just service revenue.

- They invest in knowledge infrastructure — capturing what their best experts know before they retire.

- They use remote and visual tools to multiply expert reach without multiplying headcount.

The companies still calling service "overhead" are running a different business than they think they are. They're running a high-volume, low-margin machine business and quietly handing the profitable half of their industry to someone else.

Key takeaways

- Service generates ~60% of profit from ~25–30% of revenue at mature equipment manufacturers

- Service margins are typically 3–4x higher than new equipment margins

- Remote visual support has been shown to cut truck rolls by ~50% (IFS)

- Treating service as a P&L — not a cost center — is now table stakes for category leadership

- The next decade of industrial competition will be won on service economics, not machine specs

Sources: BCG / Aberdeen Group via PTC industry analysis; IFS case study on remote triage and truck roll reduction.

What if service became your highest-margin business line?

See how manufacturers are turning aftermarket support into compounding profit.

Related Articles

AI Is Only Intelligent When Humans Give It Context

Read article

Industrial Experts Are Stuck Using Office Tools That Don't Solve Their Problems

Read article